The next frontier in group health insurance plan designs

Carriers and employers are exploring health plan designs that aim to better manage costs and streamline access to care for employees.

To understand where health plan designs are headed in the future, it's important to look back a few years to see how the global pandemic helped shaped the health plans of today.

In the first half of 2020, as organizations found themselves rapidly moving to remote work models, business leaders saw a fundamental shift in the “balance of power” from employers to employees. Attracting and retaining talent became more challenging. And, as employees demanded more from their benefits package, employers turned to their carriers for solutions to help them attract and retain talent.

Now, with the employer/employee dynamic tilting back to pre-pandemic “normal,” employers once again find themselves reevaluating their health plan strategy, seeking options that help them manage costs without limiting choice or other elements employees have grown to appreciate and expect over the past couple years.

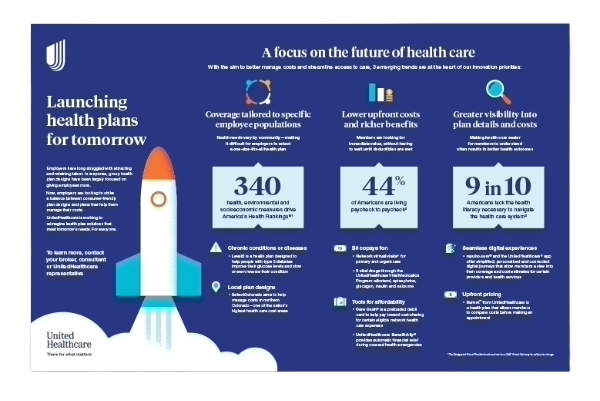

A one-pager on health plan design

Learn how UnitedHealthcare is working to reimagine health plan solutions that meet tomorrow’s needs for everyone.

For instance, the health plan designs of tomorrow are likely to offer expanded coverage with reduced member responsibility for costs, access to more convenient care options, upfront pricing for health care services, lower costs aligned with quality providers and facilities and simpler digital and mobile experiences.

When it comes to reimagined health plan designs, these 3 trends are gaining traction:

Offering more coverage and lower upfront costs

Moving forward, health plan designs may cover more upfront costs to help make it easier for employees to pay for preventive or routine care before they meet their deductible. This provides more perceived plan value right from the start: Members feel like their health insurance is kicking in immediately instead of paying 100% out-of-pocket until a deductible is reached.

This matters, because plans that don’t offer these upfront cost-savings may leave employees feeling frustrated or questioning why they pay for health insurance at all, especially if they don’t reach their deductible by the end of their plan year.

Where savings and support meet

“At UnitedHealthcare, we’re developing health plan designs that balance simplicity and affordability. We believe we’re moving in the right direction by combining the cost-saving power of programs like Care Cash, the Vital Medication Program, $0 24/7 Virtual Visits and Benefit Ally with a more personalized experience,” says Kelley Nolan-Maccione, chief product officer for UnitedHealthcare Employer & Individual.

Plan designs that offer $0 copays for designated services or that are void of deductibles or coinsurance may help employees feel like they are getting more out of their health plan.

Additionally, pairing those plan designs with products like Care Cash from UnitedHealthcare — a preloaded debit card designed to help employees pay for their portion of certain eligible network health care expenses — may also make a difference.

Providing greater visibility into cost and quality

Layering price transparency into plan design is another step many carriers are taking. Giving employees more insight into the cost of care and aligning lower costs with quality providers may help members make more informed decisions.

Many carriers like UnitedHealthcare are also weaving algorithms into their digital experiences and provider search engines that prioritize providers who have a history of delivering quality care and positive health outcomes — and then sorting those quality providers based on average cost of care. This empowers employees to choose a provider that can best serve their health needs while staying in budget.

“Consumers want their health care experience to match their other online experiences — easy to navigate, transparent pricing, easy-to-access reviews, secure purchasing and quick delivery,” says Samantha Baker, chief consumer officer for UnitedHealthcare Employer & Individual. “During a time where costs are rising everywhere and there are many options, UnitedHealthcare is focusing on simple, personalized, digital-first plan designs and product offerings to give control back to the consumer.”

Consider a plan like Surest™ from UnitedHealthcare. Through a digital experience designed to be easy to use, members can check cost and coverage information for specific procedures, treatments and services before scheduling an appointment, with lower prices indicating providers evaluated as higher value. This pricing model allows for a shift in how we think about value, factoring in efficiency, safety and effectiveness such as improved outcomes, lower likelihood of surgery complications, efficient use of resources, service costs and more. That level of transparency can give employees greater control over their health care experience and their costs.

- 54% lower average out-of-pocket costs for Surest members3

- Up to 15% lower employer costs on average with Surest3

A plan design that takes this model a step further

As the health care ecosystem becomes broader, more disruptors are coming onto the scene, creating health plans that aim to address some of the same challenges UnitedHealthcare is working to solve. “We continue to look for opportunities to accelerate what we’re already doing by working with others and entering into agreements with other entities within the health care system,” Alberti explains.

For instance, UnitedHealthcare is working with Garner Health on a health plan addition that uses data science to assess the performance of providers with the goal of improved quality of care and affordability for covered employees.

Garner’s provider analytics and Health Reimbursement Accounts (HRAs) incentivize covered employees to select quality, network UnitedHealthcare providers. When a member selects a provider evaluated by Garner, the health plan contributes to the member’s Health Reimbursement Account (HRA). This may result in improved outcomes and a lower cost of care.

Tailoring coverage to specific employee populations

Because health needs can vary greatly from community to community, employers may find it difficult to select a plan design that meets the needs of their entire employee population. As a result, many carriers are looking at communities or pockets across the country that may be experiencing worse health outcomes, higher costs or more barriers to care than others and designing health plans that aim to help a specific population.

For instance, northern Colorado was identified as one of the nation’s highest health care cost areas. To help manage those costs, UnitedHealthcare teamed up with 2 major health systems — UCHealth and SCL Health, now part of Intermountain Health — to build a new health plan called SelectColorado. This health plan is designed to give members better access to quality network providers across 14 counties, with $0 copays for 24/7 Virtual Visits, primary care office visits, urgent care visits and behavioral health visits.

Health plans like these exist across the country. In fact, in many cases, carriers pilot different health plan designs within specific markets to determine whether it has the potential to be effective for a broader population. At UnitedHealthcare, examples of this include the Charter plan offered in Chicago, Houston and Dallas; Doctors Plan offered in Arizona, Colorado, Northern California and Washington; NexusACO® plans offered in Chicago, Louisiana, Oregon, Texas, Virginia and Washington; among others.

“My colleagues and I often discuss how our regions approach health care in different ways. Yes, there are many common denominators, but it’s the differences we want to provide for within our overall parameters. Those differences could be influenced by cultural diversity, economic factors or even access to care,” explains Rob Henderson, regional vice president of product for UnitedHealthcare Employer & Individual.

This same idea of tailoring health plans to specific employee populations based on where they live can also be applied to those who are dealing with different chronic conditions or diseases.

For example, Level2® is a health plan designed to specifically address type 2 diabetes. Through a combination of wearable technology, clinical support, coaching, lifestyle changes, personalized support and incentives, this plan aims to help employees improve their glucose levels and slow or even reverse their condition. Plus, self-insured employers benefit from guaranteed savings and contained medical costs.

“Wearable technology provides data that is directly tied into a person’s health status and allows them deeper insight into their physical health. When members share this information with us, it allows us to connect them with personalized programs, like Level2 for type 2 diabetes,” explains Brad Anderson, chief strategy officer for UnitedHealthcare Employer & Individual. “It’s the intersection of data, clinical insight, coverage and incentives that enable us to get better health outcomes for our members.”